How to keep your retirement plans front and centre amid the cost of living crisis

With the cost of living crisis now in full swing, it may have you concerned about the prospect of your retirement plans.

Surging inflation, rising interest rates, and continuing market volatility are all contributing to financial uncertainty for many people in the UK. As a result, you might have found that your money doesn’t stretch as far as it did before.

While you might be able to cope now, this can be a worry if you’re intending to retire in the near future. After all, if you have less money to support yourself now, it seems likely that you’re going to find yourself in the same position in retirement.

The knock-on effect of this could be anything from not being able to live the retirement lifestyle you really want, to even having to rethink your plans entirely.

If you are feeling like this, then you’re far from alone. Find out why, and how working with us at Britannic Place ensures that your retirement plans remain front and centre.

30% of over-55s have already made changes to their retirement plans

The effects of the cost of living crisis are beginning to make their mark for pre-retirees, forcing many people to rethink their post-work lives. That’s according to research conducted by Royal London and reported by Professional Adviser in November.

Royal London found that 39% of over-55s surveyed said they were concerned they would not be able to reach their retirement goals. Similarly, 38% of respondents said that the current economic situation was leading them to worry that they wouldn’t have enough money in retirement.

Concerningly, this has led to 30% of respondents already making changes to their retirement plans, including an increasing number of people who were debating whether to consider working in retirement to afford their lifestyle.

These effects are also being felt by individuals seeking a slower, phased retirement, according to research published in MoneyAge that was carried out by Legal & General.

This survey revealed that 40% of over-55s who were planning to gradually retire over the next five years were now worried that their plans would be thrown into jeopardy by the cost of living crisis.

3 handy tips to help you stay on track towards your goals

Amid these difficult economic circumstances, you may well fall into one of these categories of being concerned about your ability to afford your ideal lifestyle in later life.

Fortunately, there’s no need to panic, as there’s still plenty you can do now to keep your retirement plans centre stage of your finances.

Read on for three handy tips that can help you to stay on track to meet your goals.

1. Reduce your spending and save more

A simple and straightforward choice you could make as costs rise now is to reduce your spending in the short term so you can save more towards your retirement.

Scour your budget and look for any areas where you might be able to cut back on discretionary spending. For example, do you have TV subscriptions you simply don’t use, or are you using up too much of your budget on social activities that you could temporarily take a step back on?

Wherever you can, try to cut back on your spending. Then, you can either save or invest this money, perhaps even contributing it to your pension to give your fund one last push before you come to retire.

Doing so could provide the additional funds you need to stay on track towards your targets.

2. Remember that market volatility is often temporary

While everything may seem rather uncertain currently, it’s worth remembering that market volatility is often temporary.

You may have anxiously been watching the value of your pension or investments fluctuate over the past few months, as stock markets have swung quite significantly.

The key thing to keep in mind is that, historically over the long term, such bumps have smoothed out and markets have eventually continued to rise in value.

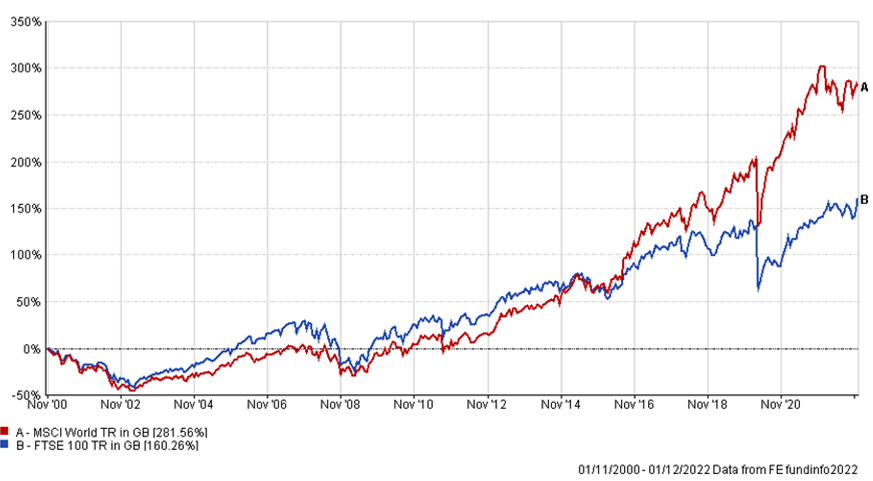

Consider this chart showing the performance of the MSCI World Index and the FTSE 100 since November 2000. Over the past 20 years, the world has been through multiple economic downturns, including the:

- Dot-com bubble, causing many markets to lose value in 2002

- Global financial crash in 2008

- Covid-19 pandemic and resulting lockdowns in 2020.

Source: FE fundinfo

Yet still, as the chart shows, the total return from these two indices has continued to rise in value over time.

That means you should try to stay level-headed where possible and avoid cutting back on your regular pension contributions and investments, or even worse, liquidating assets to tie you over in the short term.

Historical performance is not a direct indicator of future performance, and you may get back less than you invest. Even so, the fact that markets typically recover from moments of difficulty and ultimately rise in value means that your pensions and investments will likely do so, too.

That’s why staying invested and steady can keep your retirement plans at the forefront of your financial decisions.

3. Speak to a financial planner

Perhaps the most sensible decision you can make is to speak to a financial planner.

At Britannic Place, we understand that it’s not always plain sailing in the markets. That’s why we build financial plans and tailor investment portfolios that take economic uncertainty into account.

By planning for uncertainty before it happens, you’ll always remain on track to meet your goals, no matter what happens elsewhere.

Above all else, we use your goals for retirement to design your financial plan. Having your ambitions at the centre means you can be confident that your plan will get you there, regardless of what’s happening outside of your control in the wider economy.

Get in touch

If you’d like help making sure that you’re on track to achieve your retirement goals amid the cost of living crisis, please get in touch with us at Britannic Place.

Email info@britannicplace.co.uk or call 01905 419890 to speak to us today.

Please note

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.